Research Disclaimer

Crypto.com Research and Insights disclaimer for research reports

Executive Summary

- Restaking extends Ethereum’s security to other systems by allowing users to stake ETH and Liquid Staking Tokens (LSTs) to secure multiple systems and earn extra rewards by committing their staked ETH for additional slashing conditions.

- EigenLayer pioneers restaking and has gained substantial growth, with over 4.7 million ETH (~US$15 billion) ready to be delegated to Operators.

- Native ETH dominated EigenLayer’s pool with over 66% share. Amongst the LSTs deposited, Lido’s stETH had the lion’s share of 61%.

- Operators in EigenLayer assist in operating AVS software. They register and allow stakers to delegate to them, providing various actively validated services (AVSs) on EigenLayer. Ether.fi commands a significant presence amongst Operators, holding over half of the total staked ETH.

- AVS is a system that requires validation and security through EigenLayer’s restaking. These systems go beyond Ethereum’s consensus and benefit from the additional security layer provided by restaked ETH. EigenDA is the first AVS with a 24% share (~1 million ETH) of staked value.

- Restaking on EigenLayer has spurred the growth of liquid restaking and the Liquid Restaking Token finance (LRTfi), with over $8 billion total value locked (TVL) at the end of April. Leading this space, Ether.fi, Renzo, Puffer, KelpDAO, and Swell collectively control 96% of the market share.

- However, EigenLayer and LRTfi face challenges and risks:

- The rapid growth of TVL could lead to a yield crisis due to a surplus of restaked assets compared to the security needs of AVSs.

- Core functions like the fee system and slashing have not been launched yet, raising doubts about yield generation.

- Other risks of EigenLayer include smart contract vulnerabilities, centralisation on Ethereum validators, and liquidity risks with LRT tokens.

- LRT tokens are susceptible to depegging and losses due to contract alterations, security breaches, and market conditions.

- The liquid restaking market is growing, with novel DeFi strategies around LRTs. Despite the challenges, EigenLayer aims to address trust fragmentation on Ethereum and holds promise for unlocking new utilities in the future.

1. Introduction

1.1 Restaking

Ethereum achieves security through a trust network built on its Proof of Stake (PoS) consensus mechanism. Validators ensure network security by staking the required amount of ETH and receive the network rewards in return if they act honestly (their ETH is slashed otherwise).

Restaking takes the concept of staking further by extending Ethereum’s foundational security to other systems. It allows native staked ETH and Liquid Staking Tokens (LSTs) to be staked with validators on other networks. Users utilise restaking to secure not only Ethereum but other systems or protocols, earning extra rewards by committing their staked ETH for additional slashing conditions.

Ethereum’s trust network allows for the construction of decentralised apps (dapps) through the programmability of the Ethereum Virtual Machine (EVM), which provides collective security for all dapps. However, certain modules that cannot be deployed or validated on the EVM are unable to benefit from Ethereum’s shared trust. These modules process inputs derived from outside Ethereum and cannot be verified within its network.

1.2 EigenLayer

EigenLayer spearheaded the restaking area and has recently gained significant market attention.

EigenLayer refers to actively validated services (AVSs) as modules that EVM can’t secure. These encompass sidechains, data availability layers, new virtual machines (VMs), oracle networks, and bridges. AVSs are typically secured by their own tokens or operate within permissioned systems.

EigenLayer addresses this limitation by enabling AVSs to achieve the same level of security as Ethereum. This advancement extends Ethereum’s trust and security to a broader array of applications and services. The workflow of EigenLayer with the example of its AVS (EigenDA) is shown below:

At the foundation of the EigenLayer infrastructure is a system enabling stakeholders to invest tokens, thereby providing economic security to each AVS. Stakers commit tokens into pools overseen by smart contracts, which subsequently delegate these tokens to Operators responsible for the AVSs’ operational security. A restaker can later initiate withdrawals, and the Operator’s slashing status is checked before the withdrawal is completed.

Initially, EigenLayer enforced the cap at 33% for any particular Liquid Staking Tokens (LSTs) to be deposited into the protocol for balancing between Neutrality and Decentralisation. After the successful launches of the first three stages, which laid the groundwork for a growing ecosystem of restakers, Operators, AVSs, and rollups, EigenLayer removed the LST caps to unleash its development.

Additionally, On 29 April 2024, EigenLayer further announced plans for a token airdrop, allocating 15% of EIGEN tokens to ecosystem participants. This participation will be distributed linearly across multiple seasons in an initiative known as Stakedrop.With the phased launch of EigenLayer on the Ethereum mainnet and introduction of EigenDA by Eigen Labs, the EigenLayer ecosystem is witnessing considerable growth. At the time of writing, EigenLayer administers over 4.7 million ETH (approximately $13 billion), poised for delegation to a variety of AVSs.

The past month has witnessed a marked increase in the deposits to Liquid Restaking Tokens (approximately +812,000 ETH) in spite of a concurrent surge in withdrawals (approximately -750,000 ETH), signifying a growing market interest in restaking solutions.

1.3 The EIGEN Token

EigenLayer announced the airdrop plan of its native token, EIGEN. Token claims and official distribution are set to begin on 10 May 2024. EigenLayer’s EIGEN token is designed to address intersubjective faults within the Ethereum ecosystem. These faults are characterised by a broad agreement among active observers of the system, such as data withholding.

The EIGEN token introduces a mechanism known as intersubjective staking, which complements the existing ETH staking mechanism by focusing on faults that cannot be resolved through ETH restaking alone. This approach allows for the resolution of intersubjective faults through a process, known as slashing-by-forking, is a last-resort option designed to ensure honest behaviour by requiring large collusion and a significant potential loss of funds. This mechanism works as below:

- Universality: EIGEN is designed to be a universal intersubjective token, capable of forking and slashing for intersubjective faults committed by EIGEN stakers across any Actively Validated Service (AVS) in EigenLayer. This universality ensures that the mechanism can be applied broadly across different applications within the ecosystem, addressing a wide range of intersubjective faults.

- Isolation: To prevent externalities that could arise from the need for applications and users to be aware of potential forks, the mechanism employs a two-token system. One token (EIGEN) is used in fork-unaware applications (like DeFi), acting as a “solid representation” that allows holders to redeem an equivalent number of tokens from any of its descendant forks at any future time. This ensures that applications like lending protocols can continue to operate without interruption from potential forks. The other token (bEIGEN) is used for staking and forking, ensuring that the mechanism can be activated when necessary without disrupting the broader ecosystem.

bEIGEN pertains to the staking layer subject to potential forking and slashing, while EIGEN serves as a DeFi-compatible representation, ensuring that protocols always interact with the latest, canonical version of the token post-fork.

- Forking Process: When a fault is identified that requires intervention, a challenger can initiate a fork of the EIGEN token. This involves committing a significant fraction of EIGEN tokens as a bond to propose the fork. EigenLayer’s social consensus mechanism then votes on whether the proposed fork is legitimate. If the fork is validated, the challenger recovers their bond and receives a reward, while tokens belonging to voters who opposed the fork are penalised. Conversely, if the consensus opposes the fork, the challenger’s tokens are burned.

- Social Consensus and Voting: The decision-making process relies on social consensus within the EigenLayer community. This consensus-driven approach ensures that the mechanism is responsive to the collective opinion of the community, allowing for the resolution of intersubjective faults in a manner that reflects the broader sentiment of the ecosystem.

- Penalties and Rewards: The fork-and-slash mechanism includes penalties for those who commit faults and rewards for those who contribute to the resolution of these faults. This incentivises honest behaviour and encourages participation in the community’s governance processes.

The introduction of EIGEN and its staking mechanism represents a significant development in the staking ecosystem, aiming to enhance security and usability within decentralised applications by addressing a unique set of challenges not covered by traditional staking methods. Additionally, the utility of EIGEN extends to easing the burden on Ethereum by handling subjective AVS faults, which could otherwise overload Ethereum’s consensus mechanism.

The total supply of EIGEN tokens is capped at 1.67 billion. Distribution includes 45% to the community, divided equally amongst airdrops, ecosystem development, and community incentives; and 55% to investors and early contributors. This latter group will experience a one-year cliff, followed by two years of monthly linear vesting. Additionally, these tokens will be non-transferable for an extended period and force geographical exclusion for residents worldwide like the US, Canada and others.

EigenLayer plans to distribute an extra 28 million EIGEN tokens to 280,000 wallets following the backlash over its initial airdrop program. The EIGEN token distribution is summed up below:

2. The EigenLayer Ecosystem

EigenLayer constitutes an intricate marketplace that mainly includes stakers/restakers, Operators, AVSs, and liquid restaking platforms. This section breaks down and explores the dynamics amongst these stakeholders.

2.1 Staker/Restaker

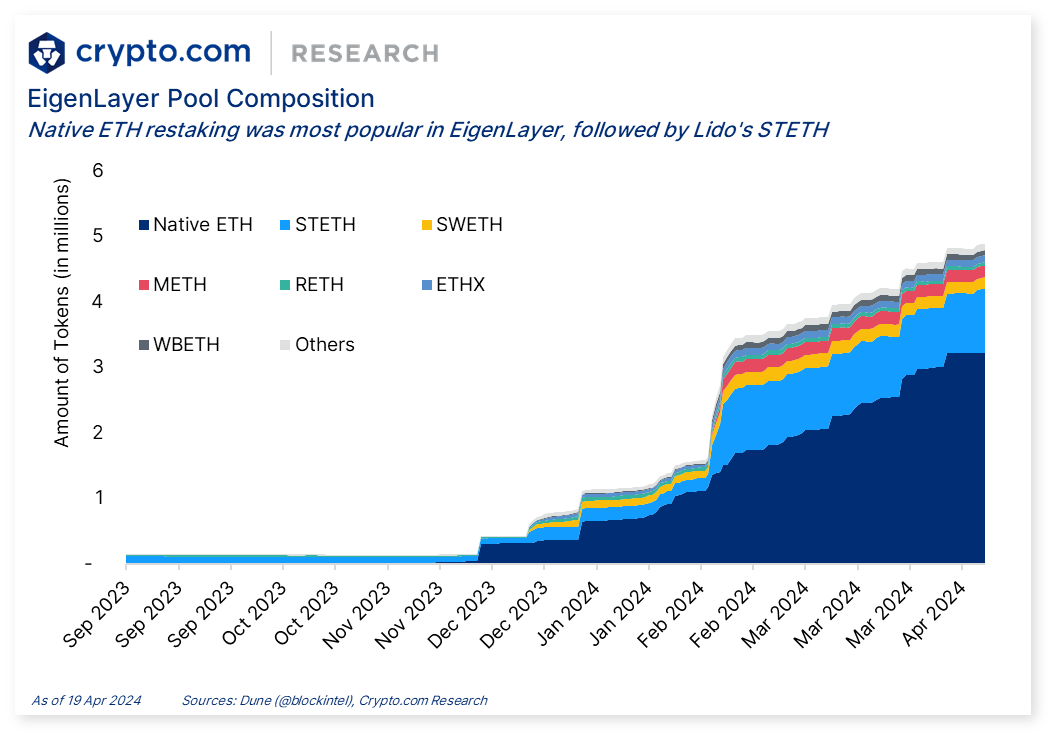

Stakers contribute tokens to EigenLayer, bolstering the economic resilience of AVSs. Their engagement involves depositing tokens (ETH and LSTs) to delegated Operators and initiating withdrawals after a prescribed period (‘unbonding period’), dependent on the status of their designated Operator. The pool composition of deposits on EigenLayer consists of 66.3% native ETH and 33.7% LST.

Amongst the LSTs deposited on EigenLayer, Lido’s stETH is the most prevalent, accounting for 61% of the total 1.7 million ETH in LSTs. This is followed by swETH (10%), mETH (9%), ETHx (6%), and wbETH (5%), respectively, in terms of market share.

2.2 Operator

Operators help run AVS software built on top of EigenLayer, registering in EigenLayer and allowing stakers to delegate to them. They then opt in to provide various services (AVSs) built on top of EigenLayer. Currently, a minimum of 96 ETH is required to become an Operator in EigenLayer.

Amongst the top 10 EigenLayer Operators, Ether.fi commands a significant presence, holding over half of the Total Value Staked (TVS). Currently, Ether.fi has 20 nodes on EigenLayer.

2.3 AVS

An AVS comprises any system that requires its own distributed validation semantics for verification and secures its system via EigenLayer’s restaking mechanism. These systems typically extend beyond the reach of Ethereum’s consensus mechanism, thus gaining from the supplementary security layer provided by restaked ETH. Node Operators on EigenLayer secure AVS transactions by restaking their ETH on the protocols, and they receive additional validation rewards on top of their staking rewards from Ethereum.

AVSs can range from sidechains, data availability layers, new virtual machines, oracle networks, bridges, execution environments, and more. Currently, AVSs in EigenLayer focus on rollup acceleration, real-world data integration, and coprocessors.

EigenDA was the first AVS developed by EigenLayer; presently, seven AVSs are operational, with more upcoming.

The total amount of ETH restaked to all AVSs is currently at ~4.7 million. EigenDA leads the share in terms of TVS, securing a significant portion of the total restaked ETH on EigenLayer with ~1 million ETH, which is 21.3% of the total restaked ETH to AVSs on EigenLayer.

Currently, not all Operators are enrolled in every AVS, with only two amongst the top 10 fully enrolled — P2P.org and CoinSummer Labs. Given that both the reward system and slashing are inactive during EigenLayer’s current phase, this could indicate a lack of incentive or necessary information for Operators to make informed enrollment decisions.

Stakers are motivated by potential yields and are likely to strategically choose Operators to stake with. However, the lack of comprehensive information on slashing and AVS rewards poses a hurdle for stakers in assessing the risks associated with selecting operators. Stakers often opt for liquid staking protocols to stake their ETH to earn yields. The liquid staking protocol issues an LST that represents the staker’s ETH staked. To earn additional yields, the staker then restakes their LST via LRT protocols. This enables them to earn additional rewards. The LRT protocols, which can hold both ETH and LSTs, have the option to either restake these assets to third-party Operators or act as Operators themselves. Operators must carefully choose and manage an AVS portfolio that balances risk and rewards for their restakers.

At present, AVSs lack mechanisms to properly incentivise participation. Typically, native tokens of AVSs generate yield from the protocol’s economic activities, which incentivises users to stake these tokens to back the protocol’s security. However, with the emergence of EigenLayer, the security model has shifted towards restaking, reducing reliance on native tokens for backing security. As native tokens are no longer primarily used for backing security, it appears they may have more limited uses, such as for governance. This shift complicates the process for AVSs to determine a sufficient and sustainable yield necessary to both incentivise restaking participants to secure their systems and engage with their services.

This competitive dynamic is expected to evolve considerably with the advent of its next phase, anticipated in the latter half of the year, when rewards and slashing mechanisms are activated. Until then, the Operator competition is likely to revolve around restaked ETH market share.

3. Liquid Restaking

With the capability of ETH restaking via EigenLayer, liquid restaking and corresponding tokens also gained traction. Similar to liquid staking, liquid restaking allows stakers to restake their LSTs to protocols to earn restaking rewards, as well as receive liquid restaking tokens (LRTs). These LRTs can be used further in DeFi protocols to maintain liquidity and seek more yields. This procedure is also called Liquid Restaking Token finance (LRTfi).

Following Ethereum’s transition from Proof of Work to Proof of Stake, the emergence of LSTs have enabled user involvement in DeFi whilst staking. LRTs advance this by providing greater yield opportunities and enhanced security contributions via EigenLayer, which bolsters Ethereum’s security across diverse decentralised applications (dapps).

As of 19 April 2024, there are approximately $3 million ETH locked in liquid restaking protocols with a TVL of approximately $8.1 billion. Ether.fi and Renzo, dominated the market with around 70% share in the TVL.

Renzo has recently seen a significant increase in market share, rising from 15% on 1 March 2024 to 33% as of 19 April 2024, primarily due to the success of its Season 1 ezPoints campaign, which concluded on 26 April. These points, awarded on a daily basis to holders of Renzo’s LRT (called ezETH), incentivise user engagement and are expected to be exchangeable for airdrops of its native tokens at a later date. The increase is also fuelled by Renzo’s targeted expansion in Layer-2 platforms like Arbitrum and Base, plus a stronger focus on DeFi integration that offers enhanced airdrop potential and opportunities for leveraged farming.

Besides the LRT protocols that directly run on top of EigenLayer, other pioneering platforms that also present the potential strategies employed on these platforms include:

- LRT Yield Tokenisation: Just as interest rate swaps fix rates in traditional finance, platforms like Pendle allow for the separation of LRTs into Principal Tokens (redeemable at maturity) and Yield Tokens (capturing the underlying yield). This enables users to lock in stable yields or engage in arbitrage.

- Synthetic Stablecoins and Leveraged Strategies: Protocols use LRTs to back synthetic stablecoins like mkUSD (Prisma) and DUSD (Davos). However, the recent trend of ‘looping’ with LRTs for recursive borrowing can lead to magnified losses if market prices dip, mirroring the high risks of leveraged strategies in other asset classes.

4. Risks and Considerations

EigenLayer launched on the mainnet on 10 April 2024, removing the limits on all Liquid Staking Tokens on 16 April. This led EigenLayer’s TVL to surge to over $15 billion (at the time of writing). However, this growth of TVL could cause a yield crisis, as EigenLayer is at risk of outgrowing the pooled security required by its AVSs, which could lead to a significant reduction in yields. This situation stems from a surplus of restaked assets ($15 billion) relative to the actual security needs of the AVSs, resulting in a mismatch between restaked assets and the security needs of the protocol. For reference, the overall TVL in Ethereum is around $54 billion, and Solana’s TVL is $3 billion.

Moreover, as aforementioned, EigenLayer’s core functions like the fee system and slashing haven’t been launched yet. This also casts doubt about the scale of yield generation from the AVSs.

In addition to the above controversies, other risks of EigenLayer include:

- Smart Contract Risk: Utilising EigenLayer’s contracts exposes users to the threat of contract vulnerabilities. Should EigenLayer’s contracts suffer an attack, funds within integrated projects may be jeopardised. Additionally, engagement with LRT protocols introduces further contract risk.

- Centralisation: EigenLayer’s demand on Ethereum validators for increased computation can unintentionally prompt network centralisation, contradicting Ethereum’s decentralised ethos. To mitigate this, EigenLayer advocates for minimal validator node requirements and the adoption of efficient AVSs like EigenDA, which demand less computational capacity, thus supporting wider network participation.

- LRT Liquidity Risk: ‘Looping’, a leveraged strategy involving recursive borrowing of certain LRTs, heightens liquidation risk. Moreover, liquidity concerns emerge if users attempt to exit LRT positions in thinly traded markets, especially if a substantial number withdraw simultaneously, potentially causing LRT values to plunge below ETH’s value.

- LRT Depeg Risk: LST and LRT tokens are susceptible to deviations from their pegged values or losses ensuing from contract alterations, security breaches, and market conditions. For example, Renzo protocol’s ezETH depegged on 24 April, causing mass liquidations on leveraged protocols.

5. Conclusion

EigenLayer’s introduction of restaking represents a significant innovation in the Ethereum ecosystem. It has successfully managed a substantial pool of over 4.7 million ETH (~$15 billion), indicating strong market engagement. Key Operators have emerged, with Ether.fi a prominent one, and new AVSs like EigenDA are strengthening the EigenLayer ecosystem. The liquid restaking market is also showing remarkable growth, with novel DeFi strategies unfolding around LRTs.

However, the ecosystem is not without its challenges. EigenLayer is criticised for missing core functionalities like the slashing and reward system in its initial launch. These features are crucial for the security model and incentive structure of blockchain projects. Meanwhile, its rapid growth has introduced the risk of yield compression, and there are concerns about smart contract security, potential network centralisation, liquidity risks, and the intricate nature of underwriting LRTs.

EigenLayer’s aim to tackle trust fragmentation on Ethereum by introducing restaking is still in the nascent stage. With the release of its core features, EigenLayer’s future holds promise, which will unlock a whole new range of utilities for its users.

Read the full report: Expanding Ethereum’s Frontier: The EigenLayer Ecosystem (An Analysis of Restaking Dynamics)

Authors

Crypto.com Research and Insights team

Get the latest market, DeFi & NFT updates delivered to your inbox:

Be the first to hear about new insights: